The debt service coverage ratio (DSCR) is a single number that determines whether a lender will finance your multifamily property — or walk away. Yet some new investors only hear about it after their loan gets flagged. By then, it’s too late to do anything about it.

DSCR measures whether your property generates enough income to cover its mortgage payments. Lenders use it to evaluate risk on every apartment building financing decision, from a 4-unit walk-up to a 200-unit complex. If your number is too low, you don’t get the loan. It’s that simple.

In this post, you’ll learn exactly what DSCR is, how to calculate it with real numbers, what lenders look for at each benchmark level, and the specific strategies you can use to improve your ratio before you submit an application.

What Is DSCR and Why Do Lenders Use It for DSCR Multifamily Loans?

The Simple Definition

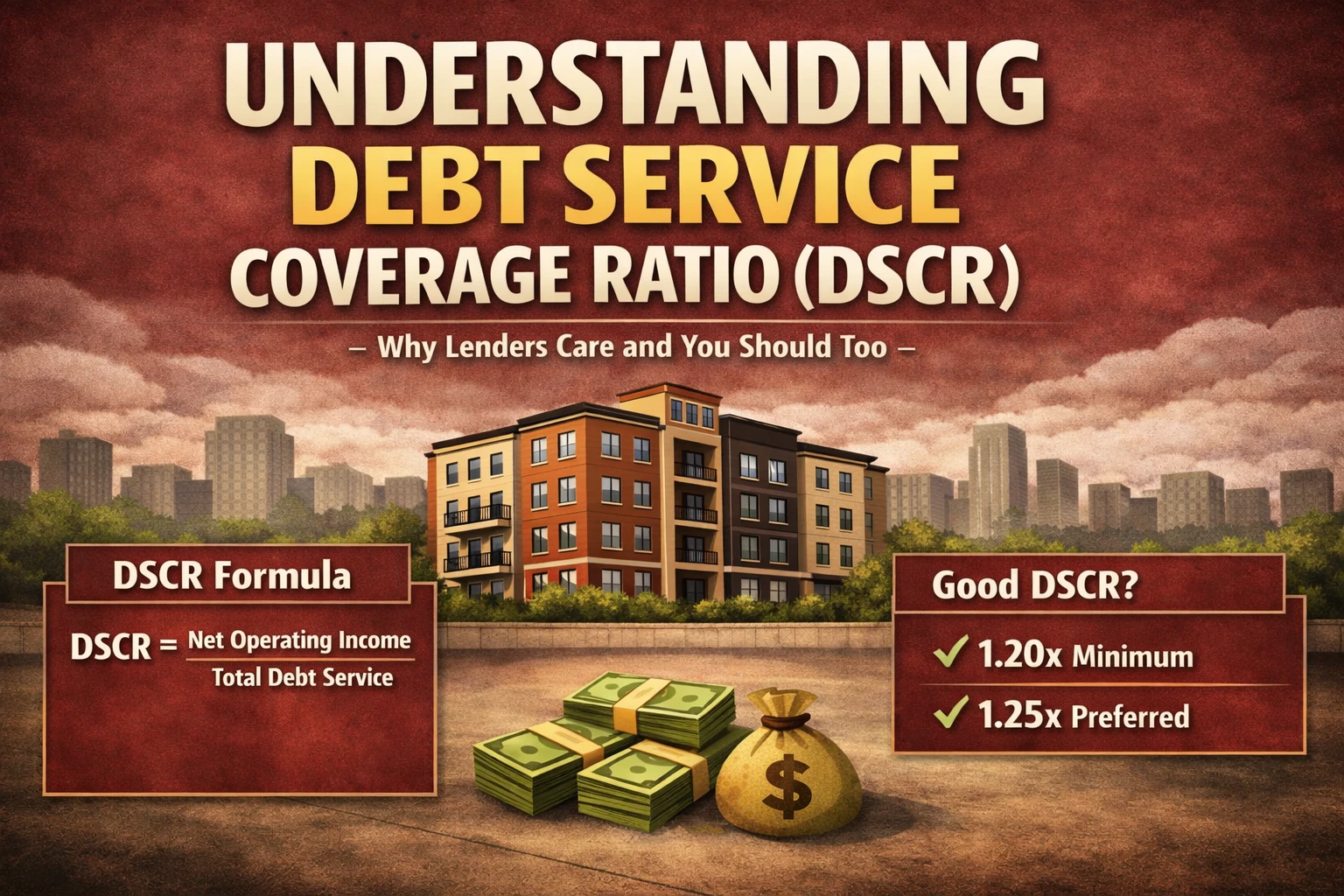

DSCR stands for Debt Service Coverage Ratio. It compares a property’s Net Operating Income (NOI) to its annual debt obligations. The formula is straightforward:

DSCR Formula

DSCR = Net Operating Income (NOI) ÷ Annual Debt Service

NOI = Gross Rental Income − Vacancy − Operating Expenses

Annual Debt Service = Total principal + interest payments for the year

A DSCR of 1.0x means the property just barely covers its debt. A DSCR of 1.25x means it generates 25% more income than needed. Anything below 1.0x means the property runs at a loss — which is an automatic disqualifier for nearly every commercial lender.

Why Lenders Rely on DSCR Over Other Metrics

Lenders don’t just want to know if a deal looks good on paper. They want to know if the property can survive a bad month. A 15% vacancy spike. A $10,000 roof repair. DSCR gives them that margin-of-safety picture in one ratio.

Unlike loan-to-value ratio (LTV), which is backward-looking (based on appraised value), DSCR is forward-looking. It tells lenders what the property will do, not what it’s worth. Both matter — but DSCR often matters more for approval.

How DSCR Applies to Multifamily Properties Specifically

Multifamily underwriting focuses almost entirely on income performance. Unlike single-family loans, lenders don’t primarily care about your personal income when you’re buying a 10-unit apartment building. They care about the building’s income.

This is actually good news for investors. A strong-performing property can qualify for apartment building financing even if your W-2 income is modest — as long as the DSCR clears the lender’s threshold.

How to Calculate Your Debt Service Coverage Ratio: Step-by-Step

Step 1: Calculate Net Operating Income (NOI)

Start with gross rental income — every dollar the building can earn at 100% occupancy. Then subtract vacancy (typically 5%–10%) and all operating expenses. Operating expenses include property taxes, insurance, property management, maintenance, utilities you cover, and any other operating expenses.

Do not include mortgage payments in operating expenses. That’s a common mistake. Debt service is separate from NOI by design — it’s the denominator in the DSCR formula, not part of the numerator.

Step 2: Calculate Annual Debt Service

Annual debt service is your total principal and interest payments for 12 months. If your proposed loan has a monthly P&I payment of $4,994, your annual debt service is $59,928. Use the actual amortizing payment — not interest-only.

Some lenders stress-test your debt service by underwriting at a rate 25–50 basis points above the actual rate. This is called a debt yield or stressed DSCR calculation. Always ask your lender which rate they’re using.

Full Worked Example: 10-Unit Apartment Building

Here’s a real-numbers example so you can see exactly how it works:

| Line Item | Annual Amount |

| Gross Rental Income (10 units × $1,200/mo) | $144,000 |

| Less: Vacancy (5%) | ($7,200) |

| Less: Operating Expenses (taxes, insurance, maintenance, mgmt) | ($58,800) |

| = Net Operating Income (NOI) | $78,000 |

| Annual Debt Service (P&I on $750,000 @ 7%, 30-yr am) | ($59,928) |

| = DSCR (NOI ÷ Debt Service) | 1.30x ✓ Approved |

Result: $78,000 NOI ÷ $59,928 Debt Service = 1.30x DSCR. This property clears the standard 1.25x threshold and would qualify for most agency and conventional apartment building financing programs.

What Is a Good DSCR?

Featured Snippet Answer

A good DSCR for multifamily and apartment building financing is 1.25x or higher. Most conventional lenders and agency programs require a minimum of 1.20x to 1.25x. A DSCR of 1.25x means your property generates 25 cents of net operating income for every dollar of annual debt service — giving lenders a comfortable safety cushion.

What Lenders Actually Look For: DSCR Benchmarks in Apartment Building Financing

The Standard Benchmark Matrix by Loan Type

Different lenders apply different DSCR thresholds depending on the loan program, property type, and market. Here’s what you’ll typically encounter:

| Loan Type | Min. DSCR | Notes |

| Conventional / Bank | 1.20x – 1.25x | Most common for community banks |

| Agency (Fannie/Freddie) | 1.25x | Standard for 5+ unit apartment loans |

| HUD / FHA 223(f) | 1.17x – 1.20x | Lower threshold, longer amortization |

| SBA 7(a) / 504 | 1.25x | Mixed-use or owner-occupied CRE |

| Bridge / Hard Money | As low as 1.0x | Reposition/Stabilization plays; higher rate offset |

| CMBS | 1.25x – 1.35x | Stricter underwriting, securitized |

These are minimums. The stronger your DSCR, the better your rate and terms. A 1.40x DSCR on an agency loan, for example, may qualify you for better pricing than a deal that barely clears 1.25x.

How Lenders Calculate DSCR Differently Than You Do

Here’s something many investors don’t know: lenders often adjust your income and expense figures before calculating DSCR. They may use lower rents than your actuals (especially if the property is newly renovated), add a vacancy factor even if the building is fully leased, and apply their own expense load rather than your historical numbers.

This is called underwritten DSCR — and it’s often more conservative than what you calculate yourself. Always ask your lender what figures they plan to use before you get too far into the process.

When DSCR Affects More Than Just Approval

A low DSCR doesn’t just kill deals — it kills pricing. Lenders may offer higher interest rates, lower loan proceeds (say, 65% LTV instead of 75%), or require additional reserves when DSCR is borderline. Improving your DSCR by 0.10x can translate to hundreds of thousands in additional loan proceeds on a larger deal.

DSCR vs. Other Lending Metrics: Understanding the Full Picture

DSCR vs. Loan-to-Value (LTV)

LTV measures how much you’re borrowing relative to the property’s value. DSCR measures whether the property’s income can support the loan. Both caps apply simultaneously — your loan is limited by whichever constraint is more restrictive. A high-value property with weak income will hit the DSCR ceiling long before it hits an LTV cap.

DSCR vs. Debt Yield

Debt yield is NOI divided by the loan amount (not the debt service). It’s a lender risk metric that doesn’t depend on interest rates — making it more consistent across rate environments. CMBS and life company lenders often use debt yield alongside DSCR. A common minimum is 8%–9% debt yield. Knowing both metrics is essential for large commercial real estate loan applications.

DSCR and the Cash-on-Cash Connection

DSCR tells lenders what they need to know. Cash-on-cash return tells you what you need to know as an investor. The two metrics are related but distinct. A property can have a strong DSCR and still produce a weak cash-on-cash return if you put in a large down payment. Always run both numbers when evaluating a deal.

How to Improve Your DSCR Before Applying for a Loan

Increase Net Operating Income

The most direct path to a higher DSCR is a higher NOI. That means pushing rents to market rate, reducing vacancy, adding ancillary income (parking, pet fees, laundry, storage), and cutting unnecessary expenses. Even a $500/month increase across a 10-unit building adds $6,000 to your annual NOI — which could push a borderline DSCR over the threshold.

Lenders want to see 3–6 months of stabilized operations, not a pro forma projection. If you’re repositioning a property, time your loan application after rents and occupancy have stabilized.

Reduce Debt Service

A lower loan amount or longer amortization period reduces your annual debt service and improves DSCR. A 30-year amortization versus 25-year can make a material difference. So can a lower interest rate — which is one reason why borrowers with strong financials and asset profiles get better loan terms.

If you’re refinancing, consider whether a partial paydown of the principal balance at closing makes sense for your deal economics. Sometimes putting in an extra $50,000 unlocks meaningfully better terms.

Use a DSCR Sensitivity Analysis

Before you ever talk to a lender, run your deal at multiple scenarios: 5% vacancy, 10% vacancy, rents 10% below current, interest rate 50bp higher. If your DSCR holds above 1.25x in the downside scenarios, you have a durable deal. If it falls below 1.0x with mild stress, you should reconsider either the price or the capital structure.

Common DSCR Mistakes That Kill Apartment Deals

Mistake #1: Underestimating Operating Expenses

New investors consistently underestimate expenses. A common error is using the seller’s stated expenses without verifying them. Budget for property management (typically 8–10% of gross revenue), maintenance reserves ($100–$200/unit/year), and realistic vacancy — even if the building is fully occupied today.

Mistake #2: Confusing Gross Income With Effective Gross Income

Gross potential rent assumes 100% occupancy. Effective gross income accounts for vacancy, concessions, and credit loss. Lenders always use effective gross income. If you submit an application using gross income, your lender will adjust it down — and your DSCR will be lower than you projected.

Mistake #3: Ignoring Lender Overlays

Each lender applies their own underwriting guidelines on top of program minimums. A bank may require 1.25x globally but stress-test at 1.30x. A credit union may cap occupancy credit at 93% regardless of actuals. Always get the specific underwriting assumptions in writing before investing time in a deal.

Conclusion

DSCR is the single most important number in multifamily lending — and now you know how to calculate it, what lenders look for, and how to strengthen it before you apply. The investors who close deals consistently aren’t lucky. They know their numbers cold before they ever pick up the phone.

Understanding the debt service coverage ratio doesn’t just help you get a loan. It helps you negotiate better terms, structure smarter deals, and avoid the properties that look good until the underwriting begins. Run the numbers on every deal before the lender does — and you’ll always be in control of the conversation.